By Mark Sprague, State Director of Information Capital

As many of you look to 2022 and beyond, we all know it’s really anybody’s guess as to what the future holds. However, many of you who know me know that I am in the business of forecasting and analysis and hopefully in the business of anticipating what comes next. (With hopefully more than 50% correct decisions on any given day.) Therefore, I have taken on topics that pertain to the housing/finance industry to get a sense of what to expect in the coming months.

Will the boom continue, or will builders/realtors start to see business plateau? Here are a few topics that need to be on your radar in your planning.

ECONOMY

Q. Will there be a recession in 2022?

No. If we look at the national economic indicators, the economy is growing slower compared to the rate we are used to over the past 18 months. Our national and regional economies would not have maintained the aggressive surge we saw. Regionally and locally, the continued job growth and economic expansion will continue to lead the national indicators. Particularly Austin and DFW. San Antonio will be healthy, and Houston will still have a challenge of recapturing the 370,000+ jobs they lost in 2022. Also, the GDP growth in 2022 will be somewhere between 3.5% to 4% nationally (3.5% to 5% is considered healthy). Potentially better in the Texas region.

Q. Will there be a housing slowdown in 2022?

Housing sales will be less because of a lack of inventory and supply chain issues. (expect 5 to 7 % fewer sales.) As stated above, the aggressive surge we saw in home sales was putting a strain on our local markets and the national markets. The good news is that job growth continues to be robust here in most of our Texas metros.

Q. Is inflation going to get worse?

It will be a mixed bag, depending on the category and industry. Some industries will see relief, while others will see continued rising prices. Wages and the supply chain are the top things to watch.

But do not expect stronger inflation to go away. If wages are increasing, that puts pressure on production and manufacturing values increasing, which in turn increases inflation. Until the globe can get COVID under control, continue to expect supply chain and production issues, which causes inflation to rise. Expect between 3.5% to 7% inflation for the next couple of years. Higher than the anemic 1.8% inflation we have seen nationally for over a decade. (Between 3.5% and 5% historically has been considered healthy.)

Q. Will we continue to see upward pressure on wages?

I cannot imagine why not. Not enough labor, nor materials.

This year, we are seeing signs of pulling away from the extended unemployment benefits, resulting in a slight increase in applications but not a total return to previous healthy employment numbers.

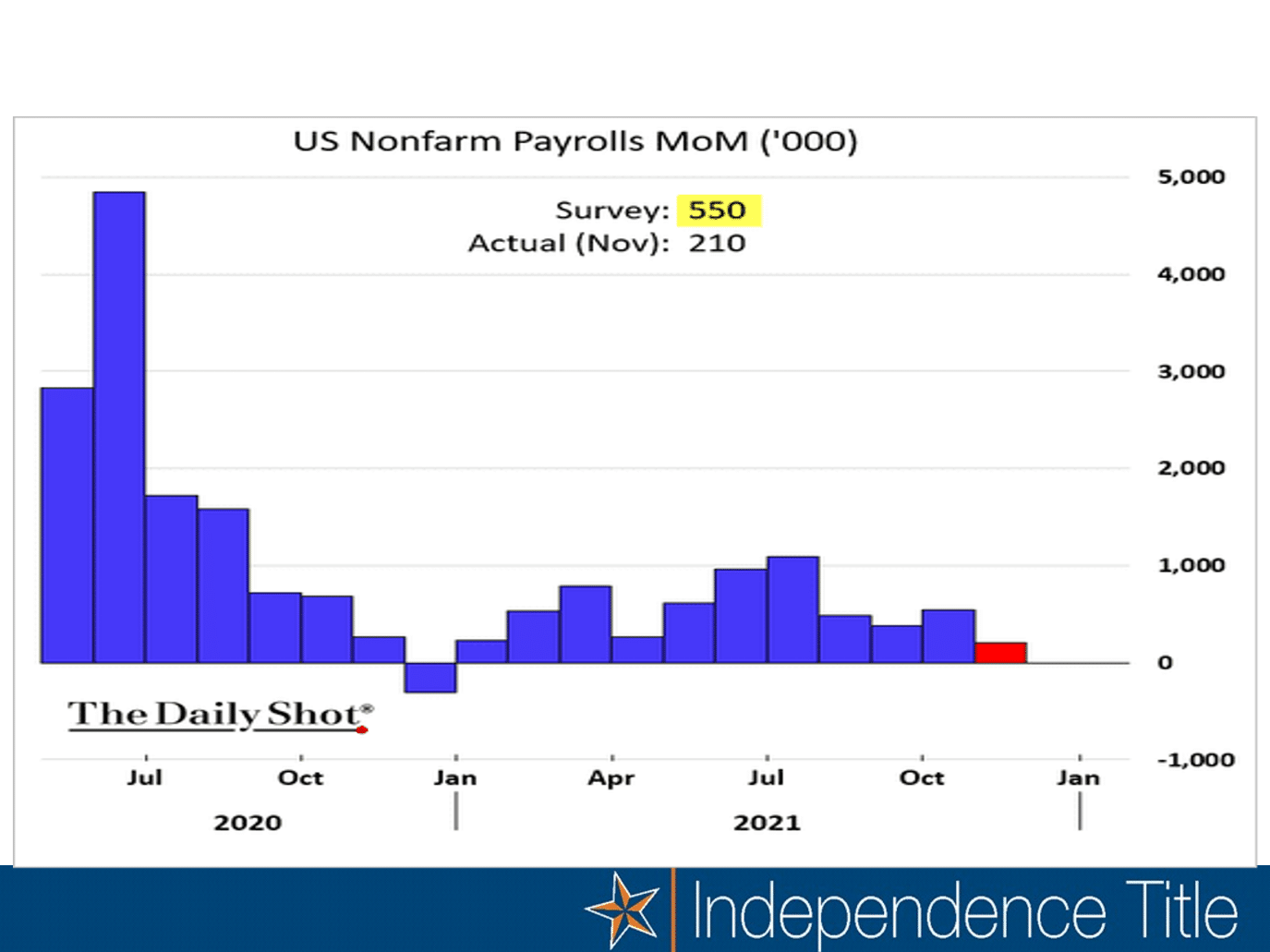

Nationally we need to return to somewhere between 750,000 to 1,000,000 jobs created and filled monthly. As you can see from the attached chart, we have been unsuccessful this year. Every time we see a new COVID variant, it slows job growth dramatically. Also, the challenge of a smaller labor pool to pull from for multiple disciplines and all likelihood should continue for several years. The good news for most of us reading is that we live and work in the Texas metros where jobs are being created in more significant numbers than the rest of the nation.

Due to the scarcity of labor, realize that workers have all the power today with record-high quit rates and a small pool of alternative employees for employers. Bigger companies that are willing to offer higher wages and competitive benefits are making it difficult for other companies to avoid raising wages if they need workers.

Not enough labor pool, yet unemployment rates continue to go down. Is this the new normal? Will we see a hybrid work model emerge?

All this is happening against an increasing inflation model.

Q. Where will interest rates end up next year? For example, will interest rates be above 3.5% at the end of 2022?

We don’t think so. When we look at the dovish attitude the Federal Reserve has taken, we don’t see interest rates above 3.5% to 3.75% by the end of 2022. However, we are tracking to see early signs of how the Fed tapering is received by investors and watching how inflation plays out to determine if we need to move our forecasts higher in the coming months.

Know that historically, when rates rise, sales in all channels pause…….hoping rates will go back down. 60 to 90 days later, everyone is typically back in as they realize rates won’t go down again. (barring a catastrophic economic event.)

SUPPLY

Q. When will we have enough housing production capability in our Texas metros to meet demand?

We believe we are at least 1.5 to 2+ years out, and even then, we may be short.

With labor as the main reason, ranging from the staff at local municipalities to workers in development, construction, and building product manufacturers domestically as well as globally. Part of this is a smaller labor pool, and the other is the challenge of COVID variants impacting workers’ lives.

Q. Is the ending of the forbearance period going to derail the housing market?

No. First, understand that the amount of slow or non-payers was less than 1% different from before the national forbearance parameter was implemented. Secondly, foreclosures historically don’t exist in a robust market. (Clarification: there will always be a small portion of any market with foreclosures issues outside the economic market issues.)

Lastly, nationally there is a significant housing deficit (at least one million+ homes), so the market should be able to withstand it.

Q. Will the majority of supply chain challenges be gone in six months?

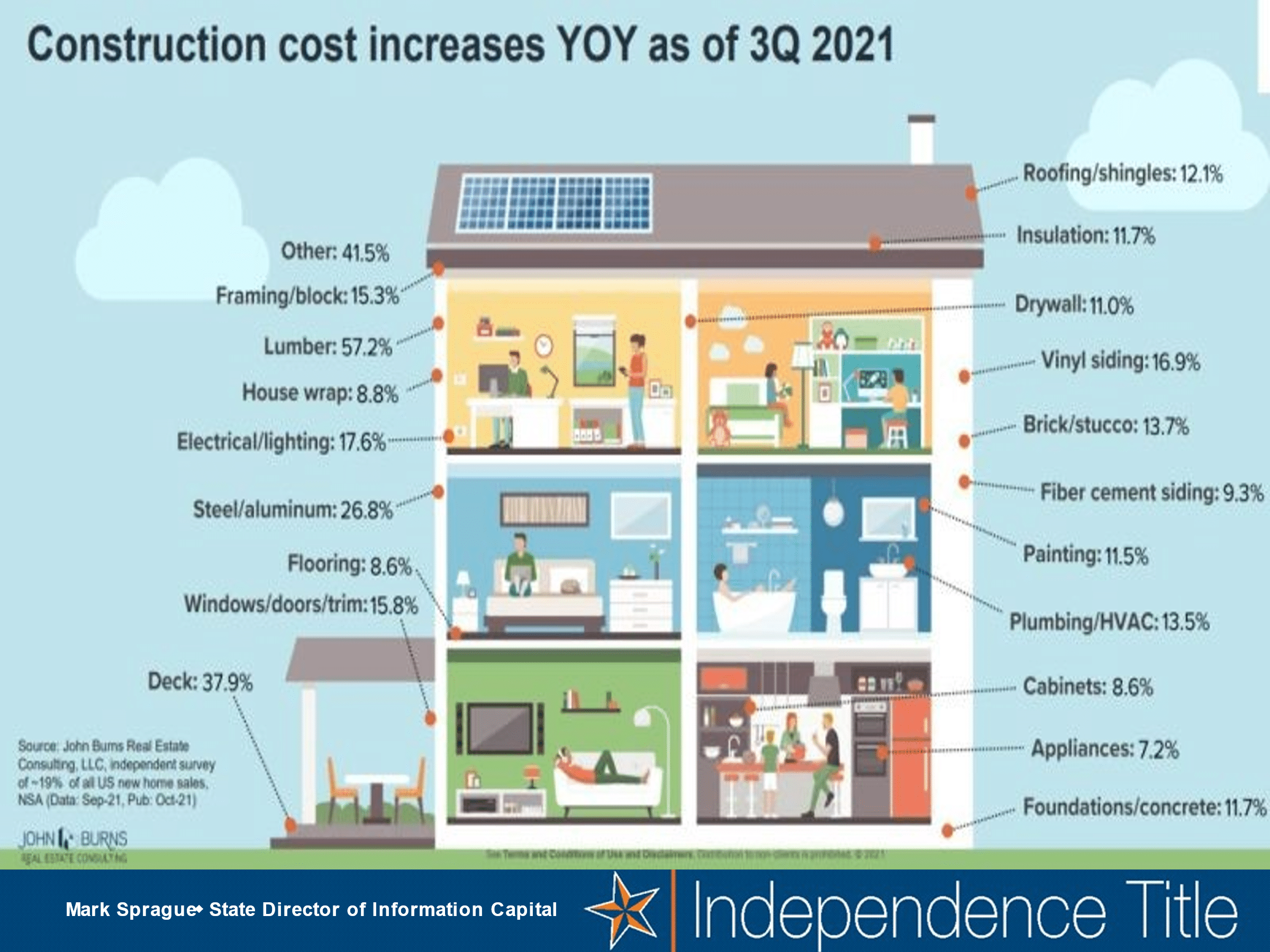

Unfortunately, not. We expect to see parts of the supply chain improve while others remain challenged on a rolling basis throughout 2022-24. Expect disruptions related to material availability and higher costs next year in all channels.

Overall building material prices have increased, up 22% during the past 12 months and up 19% year to date (including energy). There are also longer delivery times. As a result, builders report shortages of cabinets, appliances, windows, roofing materials, etc.

Q: What about commercial real estate?

Nationally and locally, it is still a tale of two economies with residential (single-family, multi-family, build to rent, etc.), industrial, and office doing well. In most of our Texas metros, a robust market needs more inventory.

At the other end of the spectrum are hospitality, leisure, and retail at less than a desirable number of occupancies and less than desirable proformas. These channels will take a number of years to recover.

Q: What about ranches and land sales?

We saw a dramatic slowdown in the first six months of last year (2020) from previous years in Texas. Yes, it was COVID-related, but the oil wars and WTI per barrel dropping to -$32 a barrel didn’t help. Ranch buyers disappeared the first of 2020. However, the second part of the year had record values due to families buying rural properties to escape the larger metros on the weekends. These purchases were driven by those families not interested in selling their primary residence and wanting a secondary or tertiary place to go with limited options because of COVID.

Land sales in Texas have been robust due to the lack of inventory in so many channels. 2022 should be more of the same.

VALUES / HOME PRICES

Q. Will we see double-digit price growth for next year?

Nationally no. Some forecasters are calling for 10% to 12% home price growth in 2022 over 2021, but it will be somewhere between 4% to 7% nationally.

Closer to home, Austin, DFW, San Antonio high single digits to possibly low teens. Houston, still recovering from the 370,000+ jobs lost in 2020, will be 4% to 6%.

Also, keep in mind that labor and material costs are rising 3% to 4% a month presently. That won’t slow down immediately. It may take a few years to address the supply chain and labor issues.

The house, apartment, and rental you look at today will either be gone or more expensive tomorrow!

Q. Will we see lending standards loosen because of the challenges of affordability?

Hopefully not. Historically bringing easier qualifying to the consumer ends up poorly for the economy and ultimately the consumers. We don’t think we’ll see adjustments to loans sold to Fannie Mae and Freddie Mac, but we already have started to see some creative solutions from private companies entering the market. But it also depends on who’s in office. With a Biden (or Democratic) administration, FHFA might make credit accessible to low-income households, but we don’t expect anything significant.

Q. To help affordability, will we see a 40-year mortgage in the next five years?

We don’t believe that Freddie Mac and Fannie Mae will likely get on board with this idea. However, the markets have become accustomed to low rates over the last 20+ years. So we do see it entering discussions to help with affordability.

Q: What are some other affordability challenges?

One of the reasons that sales and rental values are continuing up is the lack of supply.

- Nationally, regionally, and locally we must increase the housing supply.

- There is a need to recruit and train workers for residential construction to do that. Not only teach these trades early in the educational process but start internships while they are in high school.

- Improve zoning and land development approval processes to enable more lots in a quicker time frame.

- Improve the building material supply chain, including a new softwood lumber agreement with Canada.

- Revaluate all tariffs on goods.

Wrap-Up → Risks for the Economy

Q: Will job and population growth continue to fuel the Texas regional market?

We believe so. Close to year-round lifestyle meets relative affordability, lower taxes, warm weather, and employment opportunities.

The number of companies the governor’s office has hosted is high. Corporations are looking for a highly educated workforce, low cost of living (that includes taxes, comparatively lower cost of real estate (to the cities we are competing for workers with) for 5+ years.

Presently, more than half of new home starts in the nation occur in the South. Weather and retirement communities help with the attraction. We believe that Texas is where California was in the early 50’s, cheap land, cheaper workforce, higher educated workforce, lower cost of living, less taxes and regulations. (i.e., meaning this market should maintain its attractiveness for growth.)

Q: What should we look for to maintain this economy?

- Job Growth – Without job growth, you have a weak economy. Locally, regionally and nationally.

- Gross Domestic Product – GDP is the blood pressure of any economy. Local, regionally, nationally. The healthy rate is between 3.5% to 5%. Too little, too much creates issues.

- Population Growth – 2.6 people per job move. For every three jobs, historically, one home starts. And so on, and so on for every dependent industry.

- Consumer Confidence – If consumers don’t believe the economy is getting better, they quit spending. A healthy consumer confidence index number is between 90 and 110. Found at the Consumer Confidence Index.

- Real Estate – We all know when real estate is doing well; how about when it’s not. When you drive through towns/cities with boarded-up businesses and homes, you know that economy is not doing well. Help wanted signs means employment locally is strong. Therefore there is a need for people to move to fill those jobs.

- Interest Rates – Rates have been abnormally low over the last 20 years due to low inflation at the same time. Rates will start inching up in 2022 / 23 as the Federal Reserve announces a tapering of MBS (mortgage-backed securities). The statement put them on schedule to hit zero new asset purchases by the end of the first quarter of 2022. Historically this would signal a raising of rates. They made no commitments for interest rate lift-off, but today’s announcement appears to set lift-off for the second quarter of 2022. They left the fed funds rate unchanged for now. The Fed is clearly concerned about inflation; therefore, rates will be raised to slow down inflation if necessary.

What the Federal Reserve will watch:

- Stimulus cliff – Will the economy notably slow in the absence of a monetary and fiscal stimulus.

- A misstep from the Fed – Policymakers are doing their best to navigate today’s environment, but we are living through unprecedented times.

- Inflation – If higher prices (and no, we are not talking about just housing.) stick with us longer than anticipated, there will be wide-reaching impacts, including higher mortgage rates.

Q: What issues do we need to be aware of over the next couple of years and further?

- Lack of buildable land – The current inventory of developed lots is at least 1.5 to 2 years behind demand, causing values to rise. (Overall inventory of vacant developed lots in the Texas metros is at the lowest level we’ve seen historically.

- Because there is a demand for developed land (so much capital is chasing and acquiring parcels in the main counties of our Texas metros and the surrounding counties), driving land values above sustainable values, as well as potentially decades supply of ‘paper lots.

- These values make hitting affordability even harder.

- We cannot always increase density in residential neighborhoods by changing the land code. Many neighborhoods deed restrictions prevent it. (Historically, courts have held up deed restrictions on land in perpetuity. i.e., land code does not change density if the deed restriction doesn’t allow it.)

We need to look at land code in all channels, particularly in the older established areas and commercial (particularly with retail and other channels evolving away from bricks and mortar), and change it to mixed-use with residential. It is perhaps giving tax credits to those commercial tracts with higher residential density.

- Affordability – With materials and labor continuing to escalate 3% to 4% a month. With rates scheduled to escalate through 2022. With the aforementioned cost of land, affordability will continue to be an issue.

- Every time the rate goes up 1%, the consumer loses 12% of buying power. ‘The house or apartment you look at today, will be gone or more expensive tomorrow!’

- Virus surges – every time we have a virus surge, it slows the economy and destroys consumer confidence. We have to get COVID under control nationally and globally to get back to normal.

- The lack of skilled labor is not going away. For most of your licensed trades (plumbers/electricians, etc.) median age is 55+ with little replacement in the wings. Lack of teaching trades (in all arenas/channels, not just homebuilding.) will continue to become more apparent in future decades. Forcing costs, etc., becomes more of an issue to our economy.

- Aging demographics – Economic history shows us that the national and global populations have always increased since forever. Since the 50’s our country and the global economy have been modeled after an ever-expanding population. Understand that during COVID, we estimated 500,000 fewer births than normal in the US. That represents an acceleration of population trends we have been seeing the last 40 years of fewer births than previous generations. Currently, we are seeing 2.1 births per couple, and just to stay even, we need to have 3.0 births per couple.

- Eleven states are growing much slower than the rest of the nation in the last 10+ years. You would not expect some New York, Pennsylvania, California, and Illinois. Ohio, Conn., Mass. New Jersey, Louisiana, Mississippi, Michigan.

- What does this mean? With fewer births and more deaths (population aging.) in 40+ years, we will need less housing, cars, groceries, etc. Fewer births obviously affect taxes, .pensions, government costs, labor pools, supply chain, etc.

All the concerns are solvable; it’s just something to be aware of in the future.

More importantly, you live in Texas, which leads the nation in population in-migration, job creation, football, etc.

Hopefully, this will give you something to help plan and prepare. Hopefully, these points will help and may create more questions or concerns. If that is you, please let us know. Contact your Independence Title Business Development Rep for help.