I keep getting these questions: “What are builders doing on purchasing lumber at these high prices?” “Any recommendations on when this will go down and how long?” and “Will prices continue to support the increase of build cost?” The quick answer is that costs will continue to go up through 2023, with a plateauing of values potentially through 2024. Then the strength of the national and global economy will pick back up.

With costs/values increasing, lending rates rise, producing a natural slowing of different value channels (real estate and other hard assets). For example, if home values appreciate 7% the next four years and mortgage rates cap out at 3.5%, that raises mortgage payments by 45%. Thus, slowing the housing markets (that does not include labor, material, and inflation costs). Historically, the market slows itself. Only when lenders have tried to ‘goose’ the market with easy lending has the market historically gotten in trouble.

Austin has weathered two catastrophic economic events in the last 15 months and continues to see the economy improve. Home values/sales will continue to improve over the next couple of years until the builder/developers/lenders catch up to demand. We will then see a slowing of values until we see another economic event.

Most of the production builders have gone to price escalation clauses in their contracts to protect themselves and sales allotment (X number of sales a week, raising values to cover costs).

Some of the reasons behind the costs…….

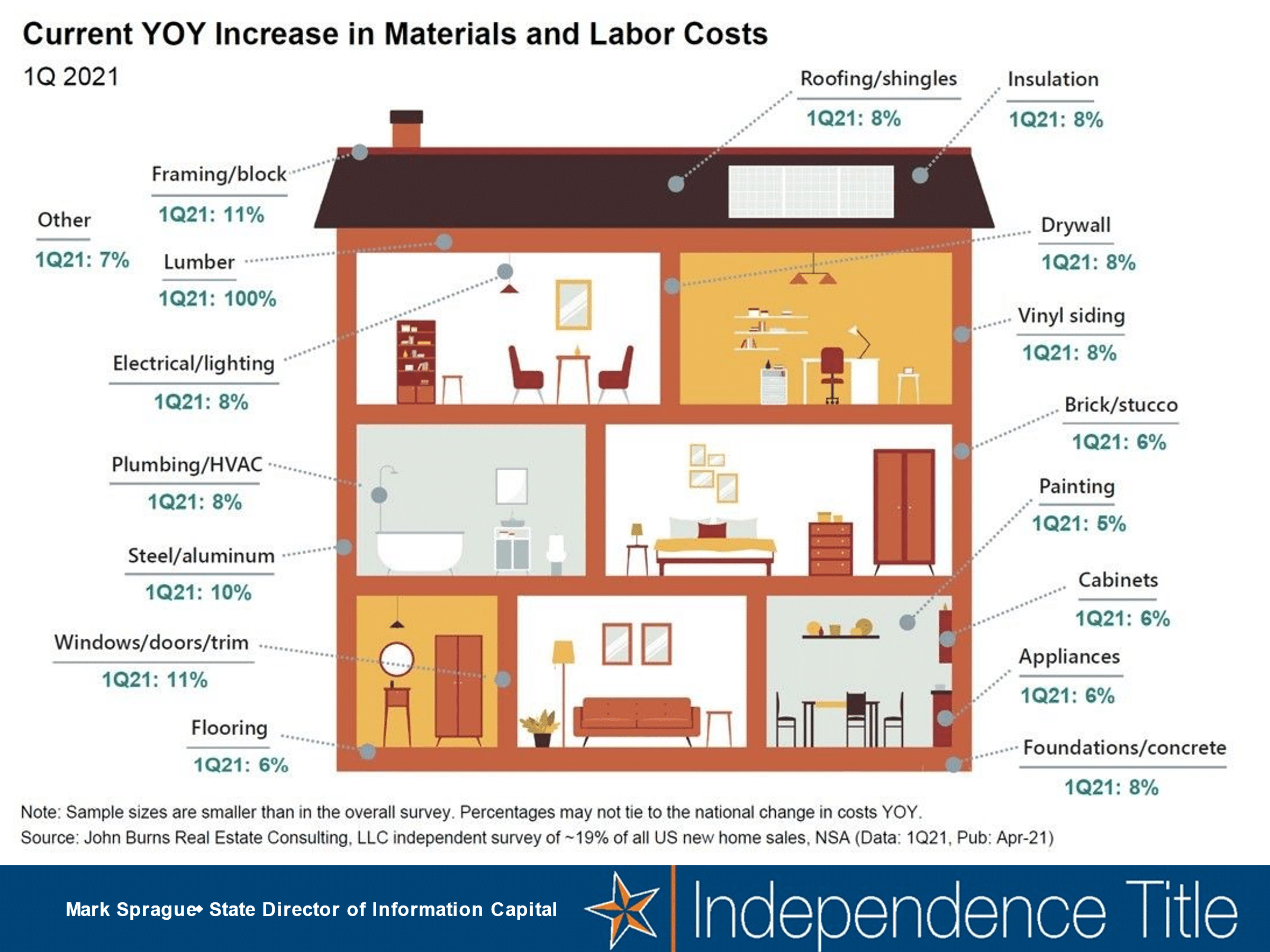

As you can see, all most all costs in homebuilding have seen costs rise. Most of this is because of increased demand. But be aware that most costs have been somewhat stable the last ten years. With demand, savings, and wages are rising, it’s increased demand, rising prices.

The original question was about lumber.

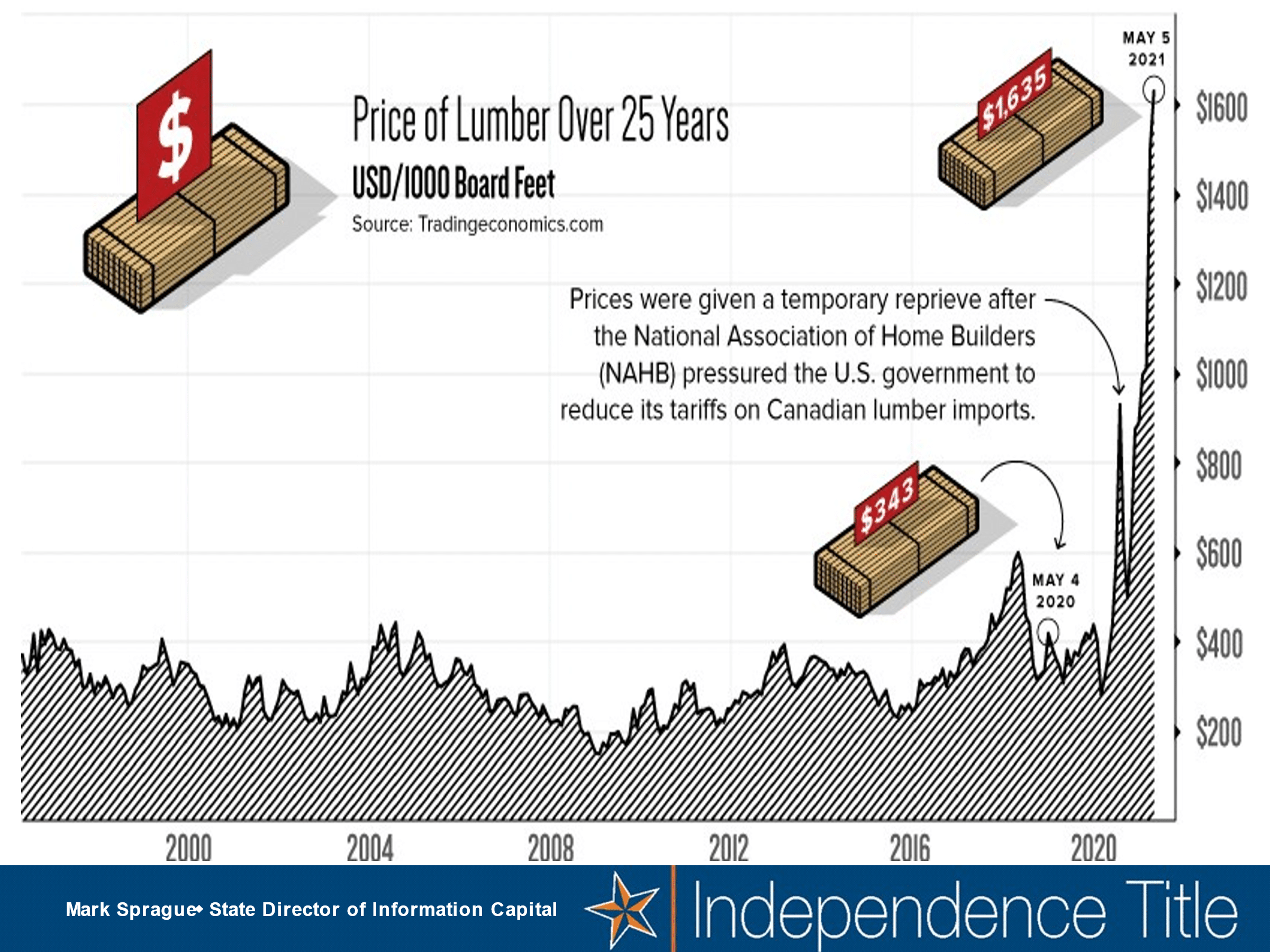

If you have been watching material futures/costs, you are aware that lumber futures posted their most significant weekly drop ($1015 a linear foot) ever last week and continued to decline. Now at <$1,000 per thousand board feet, prices are down almost 41% since May’s record high.

What’s going on? Demand for homebuilding across North America strained supplies, skyrocketing prices. But sawmills have increased output (+5% over the last year, and another 5% increase is expected ahead), and now more buyers are balking at historically expensive wood. For context: Since the early ’90s, lumber futures have mostly traded between $200 and $600.

Is higher-priced lumber the new normal? Lumber market experts think so—at least for the next couple of years. Strong demand and lack of new mills will probably keep lumber prices above pre-pandemic levels for at least 1–2 years.

Why will lumber stay high for a while?

Lumber and plywood prices have jumped 6 times in the last 15 months and slowed temporarily. Cost of material and labor has been rising 3% to 4% monthly the previous two years. Experts feel they will start to plateau towards the end of 2022. Slow at that point and then pick back up.

The reason is that demand picked up dramatically during COVID due to DIY demand and surprisingly more robust housing demand. Realize as the chart shows that lumber values had been relatively stable for over 20 years.

In that time, we lost several mills due to consolidation and cost. COVID exasperated the situation with mill closures (devastating economic effect on those small rural communities) with little to no capability to restart due to loss of labor and cost. The cost ($150 million+, two years out, lack of solid ROI, and ability to build new mills prevents new mills from being made, plus you have lost your labor (they’ve moved away to better-paying jobs.). The lumber mill industry currently maxes out at 1.5 million linear feet a day (demand is presently at 1.7 million linear feet a day).

Wood products companies would like to add capacity, but a new mill takes about two years to build. Before the pandemic, many new mills were being constructed as production shifted from Canada to the South. Why? A plague of tiny mountain pine beetles, no bigger than a grain of rice, have already destroyed 44 million acres (15 years of log supplies in British Columbia, enough trees to build 9 million single-family homes, and are chewing through forests in Alberta and the Pacific Northwest.) In addition, the construction of the new southern mills in 2018 and 2019 led to long lead times for mill equipment. Therefore, building a new mill today would probably take more than two years.

Producers are trying to increase the output of existing mills, but labor is a challenge for most. A few Covid-19 outbreaks among production workers disrupted production. Mills also are challenged in hiring new workers. In addition, there has been a long-term trend away from blue-collar occupations, partly due to educators telling high school students they have to go to college. On top of that, mills are located in rural communities that have been losing population. Finally, the stimulus checks and unemployment insurance bonus payments have sapped some people’s interest in taking jobs.

On top of the direct labor challenges, truck drivers are vital to our economy, particularly wood production, starting with moving logs from forests to mills and then getting finished products to distribution centers and lumberyards. Unfortunately, truck drivers are in short supply across the economy (we are short about 27+%). Glue shortages caused by the winter storm-related shutdown of petrochemical plants in Texas also lowered plywood production, but that’s a temporary problem.

Wood is relatively abundant, in North America, especially in the southern forests. Modern mills are very efficient at turning logs into 2x4s and sheets of plywood. Lumber and plywood prices are so high now because of the short-run dynamics of demand and supply.

Wood products prices typically fluctuate more than most goods because homebuilding can move up or down much faster than sawmill capacity can. In addition, wood products have other more stable uses, such as non-residential construction, crates, and pallets. Still, new housing is the most significant usage, followed by home repairs and remodeling, and both of those activities are highly cyclical.

Wood demand shot up in the summer of a pandemic. Many homeowners were stuck at home, unable to vacation, saving money. With time and money on their hands, they headed to the local building supplies dealer for the materials to build decks, playhouses, she-sheds, man-caves, zoom rooms, and additional rooms, etc. Also, they had a ton of money saved. Savings quadrupled during COVID. From $2.5 trillion to over $9.5 trillion.

In the Fall of 2020, homebuilders cranked up their construction. By December, single-family housing starts (seasonally adjusted) hit their highest level since 2006. This activity was driven by historically low-rate mortgages, driving payments down as interest rates dropped in the early days of the COVID pandemic. After that, mortgage rates fell slower, but eventually, 30-year fixed-rate mortgages dropped under three percent, hitting record lows.

The low mortgage rates and more considerable savings brought more buyers into the single-family real estate market. Working remotely persuaded a few long-time apartment dwellers to buy houses, but the vast impact came from families that had anticipated buying a home in a few years. With extremely low mortgage rates, purchases penciled out in 2020 and 2021.

These constraints mean that increased supply won’t bring prices down any time soon. It also explains why values rose so sharply in the past year.

Lumber and plywood prices will drop as demand falls. At some point, most of the people who can take advantage of low mortgage rates will already have bought a house. And interest rates will eventually rise (I predict mortgage rates will increase in the later months of 2021 and more rapidly throughout 2022, but many economists/analysts see more muted increases). Thus, by the end of 2023, the substantial increase in demand for housing will be over. At that point, lumber and plywood sales will drop to more normal levels.

Most housing and housing products executives see current demand as a return to normal rather than abnormally high. For example, housing starts averaged 1.5 million units per year from 1960 through 2010, but the last decade has been below that benchmark.

That reasoning fails to consider population growth, the most significant driver of housing demand. Over that earlier period, population growth averaged 1.1% per year. Over the past decade, however, our population growth was just 0.6%. In the 1960-2010 era, the number of households grew by 1.3 million per year. In the last decade, growth averaged only 1.1 million homes. And population growth has slowed more in recent years because of very low immigration. With lower population growth and households, the historical 1.5 million housing starts is reasonable for a boom year, not an average. If we look at future population growth, there is a concern. If we take out Asian and Hispanic births from the national equation, we are declining by 2025.

Developers/builders/lenders had been conservative since the downturn over ten years ago. During other recessions, the concerns about business failures were high on everyone’s lists, including the regulators and lenders. The overbuilding and easy lending that caused the last downturn was not going to happen again. Most new homes available were what we call “just in time delivery.” The wasn’t a large amount of inventory available coming into the COVID recession, and there weren’t plans to have a lot coming out.

Most cities saw their employment markets slow during COVID, Austin, DFW, San Antonio, and much of Texas did not. But, as we all know, locally significant employment news happened. Oracle, Tesla, Elon Musk, and the many interests and subsidiaries and suppliers began relocating/expanding in the Austin area. In addition, DFW and San Antonio have seen continued expansion throughout 2020 /21.

Job creation is the basis of any good economy. Austin, DFW, San Antonio, gets an A+ for job creation last year and into the future with all the expansions and relocations. However, it will take a couple of years, at least for Austin developers and builders, to catch up.

Finally, lumber and plywood prices typically rise in the spring and drop by the end of fall by about five percent. This year, look for not a decline but a leveling off. Prices will remain high for another two or three years, then drop back to more normal levels. The key to the pace of decline will be mortgage rates. In the meantime, homebuilders will pass the costs along to their buyers. The do-it-yourselfers will have a good excuse to postpone new projects. What better time to take a vacation? Think about what is getting ready to happen in that arena/channel, which, in turn, is suitable for Texas tourism.

Should you have any other questions/concerns, let us know. Another good source of what is happening is Independence Title’s economic market updates. Contact your Independence Title Marketing Rep if you have any interest.

Sources:

Why Lumber And Plywood Prices Are So High—And When They Will Come Down

AN ECONOMIST EXPLAINS SKYROCKETING LUMBER PRICES

Boston Real Estate News: What will it take for lumber prices to come down?