By Mark Sprague, State Director of Information Capital

Jobs nationally and locally continue to be created at a robust pace. (Job openings are twice the number of people out of work nationally and locally.) Consumers are spending. Businesses are investing. The housing market has slowed largely because of a lack of supply rather than a drop in demand. It is hard to see any significant slowing in growth or inflation rate. Many economists, analysts, and the media are once again underestimating the strength and resilience of the U.S. and Texas economies. The reason for that appears to be that they focus on the increase in nominal rates and ignore what is happening to real rates. As long as real interest rates remain negative, the economy will not slow by any appreciable amount, and inflation will remain stubbornly high.

Mortgage rates – The U.S. has been experiencing all-time low mortgage rates for almost two years. But now, that is changing.

Low mortgage rates are usually a sign of a struggling economy. Rates plummeted in 2020 when COVID began. People lost jobs, businesses closed, many companies were unsure of the future, and the Federal Reserve lowered the Federal funds rate to 0% and .25% to help the economy. They stayed at those mortgage rates throughout 2020 and 2021.

As the economy begins to heal, mortgage rates have started rising at the beginning of this year, 2022. Yes, the economy is still recovering from the damage caused by the pandemic. However, we’ve successfully added jobs, more people are joining the workforce, and inflation has increased.

These trends can be good for an economy, but potential homebuyers are upset they can no longer get a borrowing rate of around 3%. (Think about it: most consumers under 40 have not seen a housing market where rates jump 2+ points in 5 months.) Mortgage rates have already gone up this year, and according to the Fed, they will continue to rise in anticipation of slowing inflation. So, the possibility of ending the year with rates between 6% and 7% is real.

There are plenty of other factors to consider, though. For example, the cost of labor and materials continues to go up 4% to 5% monthly, making the house or apartment you look at today more expensive tomorrow. However, if there are more waves of COVID variants globally, if the Russian-Ukraine conflict continues to impact the global economy negatively, and China’s economic growth continues to sputter, the U.S. national economy could slow, and the rise in rates might stall …(I wouldn’t hold my breath…..the house, the mortgage is still going to be more expensive.)

The Fed plans to raise the funds rate from 0% to what it believes is a neutral rate of 2.5% to 3%or so by the end of this year and perhaps even move it slightly above that neutral level into the restrictive mode in 2023, which means that lending rates will be closer to 6% by the end of 2022 and 7% 2023. Naturally, this has affected stock market investors and caused economists to ratchet their growth expectations downwards. But the Fed told us what it planned to do in December of last year (2021), and the stock market has been sliding steadily ever since. So, it seems reasonable to see clear evidence of slower economic activity.

We are coming off a tumultuous two years of solid growth in the U.S. housing market. And now, we are facing a tumultuous year of mortgage market normalization. Interest rates are rising, affordability is challenging, and geopolitical conflicts impact global supply markets.

Lastly, you shouldn’t wait to buy based solely on interest rates. They will continue to increase, but they are still historically low. If you want to buy, waiting will cost you! Every time rates go up; you lose buying power. However, while a higher interest rate will increase your monthly payment, the change may not be as dramatic as you might think. Higher rates have not stopped sales historically. (Historically, rate increases pause the market for 60 to 90 days, and then activity picks up again.)

So, all the above is happening, right? It’s all about perspective………..

The Slowing Housing market – Many of you point to the national and local housing market as evidence that slower growth has arrived. Existing home sales seemed to slow at the exact same time that the Fed began to sound tough and the stock market began its swoon. Most of us (including economists and analysts) conclude that the housing market is slowing down in response to the combo of sharp increases in home prices and rising mortgage rates. It makes perfect sense. Or does it?

Let’s look at the Texas metros in 2022.

DFW Market facts. Here is an update with year over year statics from May 2021 to May 2022:

- Median sales price: up 22%

- Days on market: down six days

- New Listings: up 19%

- Sold Listings: down 37%

Active listings in DFW are 53,764, up 26.2% (Time to worry, right? Not!! DFW still has less than two months’ inventory.)

The average List Price is $362,200.

Inventory is now 1.5 months which is well below a balanced market of 6 months.

San Antonio Market facts: Here is an update with year over year statics from May 2021 to May 2022:

- Median sales price: up 24%

- Days on market: down seven days

- New Listings: up 37%

- Sold Listings: down 2%

Active listings in San Antonio are 6029, up 37% (Still less than two month’s inventory)

The average List Price is $347,530.

Inventory is now 1.6 months which is well below a balanced market of 6 months.

Austin Market facts. Here is an update with year over year statics from May 2021 to May 2022:

- Median sales price: up 19%

- Days on market: up 5.4 days

- New Listings: up 24%

- Sold Listings: down 37%

Active listings in Austin are 2761, up 52% (Again, still less than one month’s inventory)

The average List Price is $550,000.

Inventory is now .8 months, well below a balanced market of 6 months.

Houston Market facts. Here is an update with year over year statics from May 2021 to May 2022:

- Median sales price: up 16%

- Days on market: down six days

- New Listings: up 9%

- Sold Listings: down 1%

Active listings in Houston are 24,301, up 9% (Just over a month’s inventory)

The average List Price is $440,670.

Inventory is now 1.3 months which is well below a balanced market of 6 months.

The Texas metro markets are shifting ever so slightly. The market has favored sellers and continues to do so. So, some are balancing out evens the playing field a little bit. After a long, harsh drought of homes for sale, we are finally seeing a tad more inventory coming on the market. So, it appears the crunch is easing a bit. Values are still increasing, however, at a more reasonable pace.

The most crucial factor is that there is less than a two-month supply of homes available for sale in some markets. Analysts, economists, and real estate agents would like to see a six-month supply for the market to be close to equilibrium. With the exclusion of Houston, the Texas metros have not been back to equilibrium for the last 5+ years. There are simply not enough homes from which to choose. Finding something that suits your needs is difficult. Home sales would be far stronger if more homes were on the market. So, have home sales suffered because of reduced demand? Or are there simply not enough homes on the market? We think it is largely the latter.

What about values? I have read that Austin, DFW, and San Antonio are overvalued markets? The media keeps quoting all these studies saying DFW is one of the nation’s most overvalued markets.

Presently, most of these studies and news stories look at a primary driver of concern, Price. Understandable, particularly when the Texas metros have had over 150+% value growth in the last 10+ years, and the coasts and most of the nation have simultaneously had 40+ to 50+% value growth. It’s easy to see shades of the previous recession, the recession before that, and so on.

But there’s a flawed logic in economics where supply and demand are paramount for finding ‘true value.’ The less product and the higher the demand, the values escalate. The values we see in many markets are because of the lack of housing starting nationally over the last 12+ years. There is a shortage of product values escalate with greater demand.

What has driven the demand in the past that resulted in a “bubble?” Speculation, relaxation of lending standards for borrowers, hype, job losses … All these would drive values up.

But these variables are not based on true demand. Many of the above parameters promote the ‘economic bubble’ theory. i.e., the bubble can burst/lose its air. The ability to lose value (deflate) quickly has to be there, and we don’t see that in our market; if the current buyer backs out, fortunately, there seems to be another waiting.

That’s how what is happening in DFW, Austin, and San Antonio is different from a “bubble” scenario. Our demand is being driven by job creation, lack of inventory, GDP into effect, historical housing permits, etc.

Also, ask yourself the question, in these overvalued markets do you see the presence of negative equity? Presently there are more buyers than sellers in our markets. Negative equity is hard to find nationally and definitely locally because of greater demand for the product.

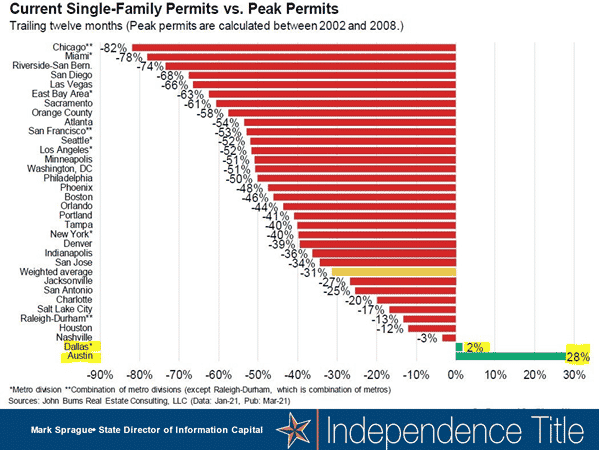

The rest of the major metros in the U.S. home starts are off -50+% to -80+%, the last 12 years. DFW and Austin are the only two national metros with more home starts, higher real estate values, employment, and higher GDP than 12 years ago. So, we are creating more jobs than we have homes; the other metros are not.

What does this mean? The rest of the nation is not creating more jobs than they have historically, slowing the number of housing permits in their metro. What does this mean for our Texas metros? It is going to take a while to catch up.

Have values dropped? The average sales price is still above the list price. All Texas metros saw peak exuberance (sales above list) spring of 2021, and all Texas metros are still averaging above list on their sold prices.

Slowing labor market? Despite concerns about a downturn, this doesn’t look like a labor market about to tip into recession. Job openings are still near record highs, and there are still 1.9 job openings per unemployed worker available in the U.S. Similarly, despite stories of layoffs and hiring freezes in industries like tech, layoffs actually hit a record low in April 2022. While DFW is particularly feeling the effect of escalating interest rates, elevated property taxes, the return to the workplace, renewed travel, and soaring gas and food prices, the good news is that all the Texas metro area’s unemployment rates are below 5% in May 2022, the lowest level since the start of the pandemic.

Overall, the fundamentals of the labor market remain robust with near record-high openings and record-low layoffs, particularly in the Texas region.

Apart from housing, there is little evidence of the economy slowing down. Retail sales through April have been rising rapidly in nominal terms and at a moderate rate after adjustment for inflation. Consumers say they are worried about what will happen, but thus far, they have not changed their consumption behavior.

Businesses continue to spend. Nonresidential investment has been climbing at a 6.0% pace, which should continue. However, with the labor market as tight as it is, firms have difficulty finding enough bodies to hire. And when they can find them, they have to offer a much higher salary than they did a year ago. When labor is in such short supply and so expensive, firms are incentivized to spend money on technology to increase output without significantly increasing headcount. For that reason, investment spending seems unlikely to slow any time soon. All the above show that inflation is here to stay for a while.

So, what is slowing if businesses are hiring and spending money on investments, and consumers are buying houses and spending money on other goods and services? Not much.

Is there a concern about the economy? A healthy national economy has an annual GDP of 3.5% to 5%. We currently expect second-quarter GDP growth of 2.0%. That may seem slow, but consider that the economy is at full employment, the amount of supply chain issues persist globally, Europe is in recession, and China is showing strong indications of a recession due to factories and cities shutting down. The U.S. had a – 1.6 growth in the first quarter. We are happy with 2% growth nationally and look to GDP improving.

If home sales are being hit by reduced demand, why does the average home sell in less than 20 days? Demand continues to outstrip inventory, so the need for housing remains solid. To be sure, some potential buyers — of houses priced at or below $250,000 — have had to change their parameters, but they still want to buy. So, they must change with the market.

So, where is the housing market?

It continues to be robust, with little change in appreciation rates over the next 3+ to 5+ years locally and regionally. Rates will continue to creep up. Rents will continue to escalate by 7% to 28% annually, pushing more renters toward buying. And still not enough inventory for rent or sale. Waiting to buy will cost you.

These are not the words of an optimist but someone who has watched housing / financial markets for nearly 50 years. If you are interested in owning a house, there is no better time to buy! Let us know what questions/concerns you may have.